⚠️ Important Notice - Please Read Before Proceeding: This article compares retirement plan options for self-employed individuals. Solo 401(k) plans (also called solo 401k plans) are specifically designed for freelancers with no employees (other than a spouse). If you have employees or are considering hiring, different rules apply. This is not tax advice—please consult a qualified tax professional before making any retirement plan decisions. Tax laws vary by jurisdiction and change frequently. Past performance of any retirement strategy does not guarantee future results.

As a freelancer, independent contractor, or 1099 worker, you're responsible for your own retirement savings. Unlike traditional employees with employer-sponsored 401(k) plans, you must choose and set up your own retirement account. Managing freelancer taxes and maximizing retirement savings requires understanding these tax-advantaged retirement plans. If you're comparing SEP-IRA vs Solo 401(k) for freelancers, both offer significant tax advantages—but understanding which one best fits your situation can save you thousands of dollars annually in freelancer taxes.

Understanding the Basics: IRA vs 401(k)

Before diving into the comparison, let's clarify the fundamental difference between these retirement account types.

An IRA (Individual Retirement Account) is a personal retirement savings account that you open and manage independently. There are two main types:

- Traditional IRA: Contributions may be tax-deductible, growth is tax-deferred, and withdrawals are taxed as income

- Roth IRA: Contributions are made with after-tax dollars, growth is tax-free, and qualified withdrawals are completely tax-free

A 401(k) is an employer-sponsored retirement plan that allows employees to contribute a portion of their salary before taxes. Traditional 401(k)s offer tax-deferred growth, while Roth 401(k)s offer tax-free growth.

The key difference for freelancers: Since you don't have an employer sponsoring a 401(k), you can either open a personal IRA or establish a Solo 401(k)—a version designed specifically for self-employed individuals with no employees.

Not sure which retirement plan fits your situation? Our team at Prefile Check can help you understand your options. Get started with free consultation →

What Is a SEP-IRA?

A Simplified Employee Pension (SEP) IRA is a retirement plan designed specifically for self-employed individuals and small business owners. A SEP-IRA is essentially a traditional IRA that allows much higher contribution limits than a standard IRA, making it one of the most popular retirement vehicles for freelancers managing their freelancer taxes.

Key Features:

- Contributions are tax-deductible as a business expense

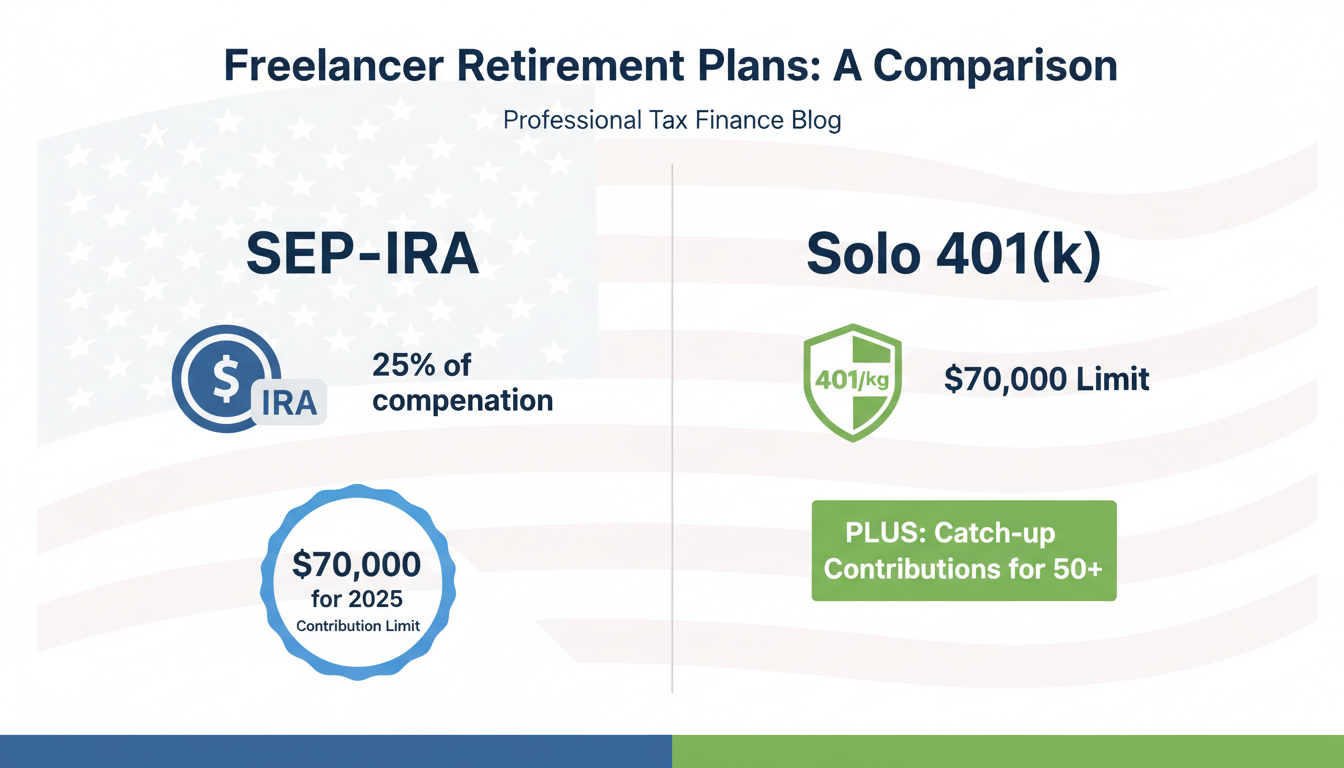

- 2024 limit: Up to 25% of net self-employment income, maximum $69,0001

- 2025 limit: Up to 25% of net self-employment income, maximum $70,0001

- No employee contributions (only employer/employee contributions as a self-employed person)

- Easy setup with minimal paperwork

- No annual filing requirements with the IRS

What Is a Solo 401(k)?

A Solo 401(k), also known as an Individual 401(k), self-employed 401(k), or simply "Solo 401k," mirrors a traditional 401(k) plan but covers only one person (plus a spouse if applicable). A Solo 401(k) is a retirement plan that allows both employee and employer contributions, giving freelancers maximum flexibility when managing their freelancer taxes.

The solo 401k option has become increasingly popular among independent contractors and gig economy workers who want to maximize their retirement savings while maintaining complete control over their financial future.

Key Features:

- Two contribution sources: Employee deferral + employer matching

- 2024 employee deferral limit: $23,000 ($30,500 if age 50+)2

- 2025 employee deferral limit: $23,500 ($31,000 if age 50+)2

- Employer contribution: Up to 20-25% of net self-employment income

- Combined 2024 limit: $69,000 ($76,500 if age 50+)2

- Combined 2025 limit: $70,000 ($77,500 if age 50+)2

- Can include Roth option for tax-free growth

- Requires annual Form 5500-SF filing if plan assets exceed $250,000

SEP-IRA vs Solo 401(k): Side-by-Side Comparison

| Feature | SEP-IRA | Solo 401(k) |

|---|---|---|

| 2024 Contribution Limit | $69,000 | $69,000 ($76,500 age 50+) |

| 2025 Contribution Limit | $70,000 | $70,000 ($77,500 age 50+) |

| Roth Option | No | Yes |

| Setup Complexity | Low | Medium |

| Annual Filing | No | If assets >$250,000 |

| Loan Option | No | Yes |

| Catch-up (age 50+) | No | Yes ($7,500 in 2024 and 2025) |

Note: Age 50+ catch-up contributions require sufficient net self-employment income to support the full employer contribution. Actual limits vary based on individual income levels.

💡 Quick Question: Are you maximizing your freelance tax deductions throughout the year? Learn how Prefile Check can help →

Choose the Right Plan: SEP-IRA vs Solo 401(k) for Freelancers

When it comes to managing freelancer taxes, choosing the right retirement plan is one of the most important financial decisions you'll make. Here's how to decide:

Choose SEP-IRA If:

When managing freelancer taxes, simplicity can be just as valuable as maximizing every dollar. The SEP-IRA offers:

1. You Want Maximum Simplicity

The SEP-IRA requires minimal administration. There's no annual filing with the IRS, and you can set it up in minutes through most brokerages. If you value your time over maximizing every tax dollar, this is a strong choice.

2. Your Income Is Very High

If your net self-employment income exceeds the Solo 401(k) catch-up contribution advantage, the SEP-IRA gives you essentially the same maximum contribution without the additional complexity.

3. You Have Employees

Unlike the Solo 401(k), a SEP-IRA can cover employees (though you're not required to contribute for them). If you plan to hire employees in the future, a SEP-IRA offers more flexibility.

Choose Solo 401(k) If:

When it comes to freelancer taxes, the Solo 401(k) offers maximum flexibility:

1. You Want to Maximize Contributions

The catch-up contribution for those 50 and older pushes the Solo 401(k) (or Solo 401k) limit to $76,500 in 2024 and $77,500 in 2025. No other retirement plan offers this much for self-employed individuals.

2. You Want Roth Flexibility

Solo 401(k) plans can include a Roth component, allowing you to pay taxes now and enjoy tax-free withdrawals in retirement. SEP-IRAs are always pre-tax.

3. You Want Loan Access

Solo 401(k)s allow loans of up to 50% of your vested balance (maximum $50,000). SEP-IRAs don't offer this feature.

📥 Download Now: Get our free Retirement Planning Checklist to track your contributions and deadlines. Download Free Checklist →

Contribution Calculation Examples

Understanding how each plan affects your freelancer taxes can help you make the right choice. Here are practical examples:

How to Calculate Your SEP-IRA Contribution

For a freelancer earning $100,000 net self-employment income:

Net self-employment income: $100,000

Less: 50% SE tax deduction: -$7,653

Adjusted net income: $92,347

Maximum contribution (25%): $23,087

How to Calculate Your Solo 401(k) Contribution

Same $100,000 income:

Employee deferral (2024): $23,000

Employer contribution: $15,349 (20% of net after SE tax)

Total potential contribution: $38,349

If age 50+: Add $7,500 catch-up = $45,849

Note: The employer contribution percentage (20% vs 25%) depends on whether you have employees and your business structure. The calculation above uses the standard 20% for self-employed individuals. Your actual maximum may vary based on your net self-employment income and specific plan design.

Why Solo 401(k) Usually Wins for Most Freelancers

As these examples show, the Solo 401(k) allows significantly higher contributions for most earners under 50. The solo 401k structure lets you contribute both as an employee (up to the annual deferral limit) AND as an employer (up to 20-25% of net income), effectively doubling your savings potential compared to a SEP-IRA at the same income level.

Tax Benefits Breakdown

Both plans provide substantial tax advantages, but they work differently:

Traditional (Pre-Tax) Contributions:

- Reduce your taxable income now

- Grow tax-deferred

- Taxed upon withdrawal

Roth (Solo 401(k) only):

- Contribute with after-tax dollars

- Grow tax-free

- Withdrawals are completely tax-free

If you expect higher taxes in retirement, the Roth option can be invaluable. If you want to lower your current tax bill, traditional contributions maximize your immediate savings.

Need help calculating your optimal contribution? Prefile Check makes it easy to track deductible expenses and plan your tax strategy. Start free today →

Setting Up Your Plan

How to Set Up a SEP-IRA

Setting up a SEP-IRA takes 1-2 hours:

- Choose a broker (Fidelity, Vanguard, Schwab all offer SEP-IRAs)

- Complete the broker's simple IRA adoption agreement

- Determine your contribution amount

- Make your contribution by tax deadline (including extensions)

How to Set Up a Solo 401(k)

Setting up a Solo 401(k) takes 2-4 hours:

- Choose a broker offering Solo 401(k) plans

- Complete the plan documents

- Open the account (both employee and employer portions)

- Set up payroll deductions if desired

- File Form 5500-SF annually if required

Important Considerations Before You Decide

Mistake #1: Missing Contribution Deadlines

For 2024 contributions, you have until October 15, 2025 (with extension). Don't leave money on the table.

Mistake #2: Incorrect Net Income Calculation

Your contribution is based on net self-employment income after deducting half of your self-employment tax. Using gross revenue will result in an incorrect, potentially penalized contribution.

Mistake #3: Forgetting the Solo 401(k) Filing Requirement

If your Solo 401(k) balance exceeds $250,000, you must file Form 5500-SF annually. Failure to file can result in penalties.

Mistake #4: Not Using Catch-Up Contributions

If you're 50 or older, you're leaving thousands of dollars on the table by not using catch-up contributions.

⚠️ Important Reminder: Solo 401(k) plans (including solo 401k variations) require that you have no employees other than your spouse. If you plan to hire workers, consult a tax professional about how this affects your retirement strategy.

Start tracking your expenses today and never miss a deductible expense. Sign up for free →

Start Planning Your Retirement Today

Choosing between SEP-IRA vs Solo 401(k) doesn't have to be overwhelming. The key is understanding your current income, your retirement goals, and how much complexity you're willing to manage.

For most freelancers earning under $150,000 annually, the Solo 401(k) (also called Solo 401k) provides superior flexibility and higher potential contributions—especially if you're 50 or older and can take advantage of catch-up contributions.

For those prioritizing simplicity or those with very high self-employment income, the SEP-IRA offers a streamlined path to tax-advantaged retirement savings.

Whatever you choose, the most important step is starting. The tax advantages of these retirement plans only help if you actually use them. Managing freelancer taxes effectively means taking advantage of these retirement savings vehicles. Set up your plan this year and start building your financial future as a freelancer.

Take action now to maximize your retirement savings.

→ Download Free Retirement Planning Checklist

Prefile Check helps freelancers and 1099 contractors track deductible expenses and optimize their tax strategy. Get started today and ensure you're not leaving thousands of dollars on the table come tax season.

Explore our guide on 15 tax deductions every freelancer should know →

Sources

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws are subject to change, and individual circumstances vary. Contribution limits and rules mentioned are based on 2024 and 2025 IRS guidelines and may be subject to modification. Solo 401(k) plans (also referred to as solo 401k plans) are only available to self-employed individuals with no employees (other than a spouse). If you have employees or plan to hire employees, different rules apply and you should consult a qualified tax professional. Employer contribution calculations depend on your net self-employment income after self-employment tax deductions. The examples provided are illustrative and your actual contribution limits may differ based on your specific income and circumstances. Solo 401(k) plans require annual Form 5500-SF filing if plan assets exceed $250,000. Failure to file may result in IRS penalties. Roth contributions and withdrawals have specific eligibility requirements that may change. Past tax benefits do not guarantee future results. Please consult with a qualified CPA, tax attorney, or financial advisor to get personalized advice based on your specific tax situation before making any retirement plan decisions. Prefile Check is not a tax preparation firm and does not provide tax advice. Any tax-related decisions should be made with professional guidance. The information in this article is current as of the publication date and may not reflect the most recent tax law changes.

Footnotes

-

IRS Publication 560: Retirement Plans for Small Business (SEP-IRA, Solo 401(k), and SIMPLE IRA Plans). For 2024, the maximum SEP-IRA contribution is the lesser of 25% of compensation or $69,000. For 2025, this increases to $70,000. https://www.irs.gov/publications/p560 ↩ ↩2

-

IRS Contribution Limits for Retirement Plans: The Solo 401(k) employee deferral limit is $23,000 for 2024 ($30,500 for those 50+) and $23,500 for 2025 ($31,000 for those 50+). Combined employer and employee contributions cannot exceed $69,000 for 2024 ($76,500 for 50+) and $70,000 for 2025 ($77,500 for 50+). https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-401k-and-profit-sharing-plan-contribution-limits ↩ ↩2 ↩3 ↩4